,

,SECTION 12.9 DETERMINE AN A0 SUCH THAT THE INTEGRAL OVER

a1x1 + ... + anxn <= a0 OF THE NORMAL EQUALS A GIVEN NUMBER (NORMPRB)

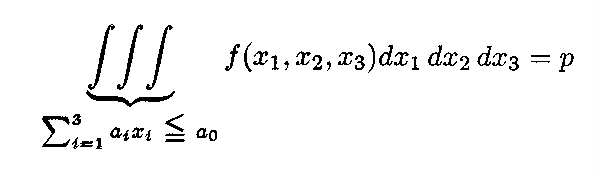

It is desired to integrate the multivariate normal density over the region given by

where the aj, j=1,...,n are given numbers. In other words, we seek the value of a0 such that ,

where f(x1,x2,x3) is the trivariate normal density. MONCARL in Section 12.8 takes the right hand side(s) of the inequality(ies) as given and calculates the probability p that a drawing from the normal satifies the inequality(ies). NORMPRB takes p as given and calculates the value of a0, for which p is the correct probability. While MONCARL can be used with any number of constraints, NORMPRB permits only a single constraint.

NORMPRB required that you specify a lower and an upper bound between which the answer will lie. If you have not provided such bounds, NORMPRB will quit and you may try again with wider bounds. If you have provided such bounds, NORMPRB will successively narrow the bounds within which the answer must lie until it is found (up to an accuracy level of ACC).

The MAIN program should include

COMMON/BPRINT/IPT,NFILE,NDIG,NPUNCH,JPT,MFILE

CALL DFLT

The call to NORMPRB is

CALL NORMPRB(ANSL,ANSH,PROB,SOL,XPROB,ACC,XMU,SIG,COV,NDIM,

* ISTOR,IER)

where

ANSL = the lower bound for the answer

ANSH = the upper bound for the answer

PROB = the specified probability with which a drawing from

the multivariate normal will satisfy the constraint

SOL = the solution to the problem

XPROB = the name of a function subprogram; must be declared

in an EXTERNAL statement in the MAIN program

ACC = the desired accuracy level

XMU = a DOUBLE PRECISION array dimensioned XMU(NDIM)

containing the mean vector

SIG = a DOUBLE PRECISION vector containing the standard

deviations of the NDIM variables if INDEP=.TRUE.

(SIG is irrelevant if INDEP=.FALSE.)

COV = a DOUBLE PRECISION array dimensioned COV(NDIM,NDIM)

containing the covariance matrix if INDEP=.FALSE.

(COV is irrelevant if INDEP=.TRUE.)

NDIM = the dimensionality of the problem (i.e., n above)

ISTOR = logical variable set = .TRUE. if NREP sample point

are to be generated once-and-for-all and reused in each

iteration, and = .FALSE. if every iteration is to

generate new sample points. The former will not only

speed convergence, but will tend to avoid unstable

oscillations. However, in this case, NREP*NDIM must

be <= 100,000.

IER = 0 for normal return, =-7 if the the bounds ANSL and

ANSH do not bracket the solution, =-67 if the

covariance matrix is not positive definite

In addition, the user must also include the following COMMON statements in the MAIN program:

COMMON/NRMPRB/A

COMMON/NRMPRB1/NREP,ICONST,INDEP

where

A = a DOUBLE PRECISION array that must be dimensioned

A(1,0:20), hence limiting the dimensionality of the

problem to 20, and where (unlike MONCARL) A(1,0) plays

no role; the values of A must be set in MAIN

NREP = the number of Monte Carlo samplings

ICONST = set internally to 1

INDEP = .TRUE. if the normal variates are independent (in

which case COV is irrelevant) or = .FALSE. if they are

not independent, in which case SIG is irrelevant